Harvestingstrength

Harvester heads

There is nothing more important than keeping harvesters up and running during harvest times. Unexpected breakdowns and repairs cost time and money, so each component must be reliable and long lasting. Some components in contact with abrasive crops require an extremely hard wearing surface and may need more than one surface treatment.

Bodycote's services help to ensure components do not wear out prematurely. Processes such as carburising, carbonitriding, ferritic nitrocarburising, marquenching and tempering may all be used to extend the life of harvesting components.

Whilst the Automotive & General Industrial (AGI) marketplace has many multinational customers which tend to operate on a regionally-focused basis, it also has very many medium-sized and smaller businesses. Generally, there are more competitors to Bodycote in AGI and much of the business is locally oriented, meaning that proximity to the customer is very important. Bodycote's uniquely large network of 127 AGI facilities enables the business to offer the widest range of technical capability and security of supply, continuing to increase the proportion of technically differentiated services that it offers. Bodycote has a long and successful history of serving this wide-ranging customer base.

Results

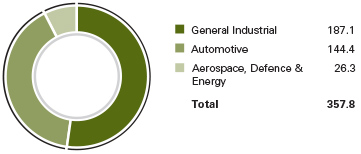

AGI business revenues were £357.8m in 2013, compared to £329.8m in 2012, an increase of 8.5% (5.7% at constant exchange rates, made up of an organic decline of 3.1% and an increase from acquisitions of 8.8%).

In 2013 sales into car & light truck have been good in all geographies with revenues increasing by 3.7% (excluding acquisitions and at constant exchange rates). Revenues to heavy truck and general industrial markets have been soft in all territories. Sales into heavy truck and general industrial sectors decreased by 14.6% and 5.5% respectively, excluding acquisitions and at constant exchange rates.

North American revenues declined by 10.2% excluding acquisitions and at constant exchange rates, driven by the softening in general industrial markets. In Europe, revenues declined by 1.7% (at constant exchange rates). In the emerging markets, revenues declined by 0.8% (at constant exchange rates), with Brazil lower by 8.4% driven by weaker demand from general industrial markets, but with Asia ahead by 18.7% helped by the Group's greenfield expansion.

Acquisitions made in 2012 increased revenue and headline operating profit in the AGI division by £29.1m and £5.5m respectively.

Headline operating profit1 in AGI was £52.7m compared to £44.1m in 2012. Headline margin increased to 14.7% (2012: 13.4%) reflecting strong cost control, particularly in areas of demand weakness and improved mix. Sales of the Group's high added-value services, and especially its S3P technology, grew strongly at high margins.

Net capital expenditure in 2013 was £34.2m (2012: £23.1m), which represents 1.0 times depreciation (2012: 0.7 times). In 2014 we expect that capital expenditure will be just above depreciation as we add further capacity in China, Mexico and for selected technologies such as S3P, Corr-I-Dur® and low pressure carburising. Return on capital employed in 2013 was 15.1% (2012: 12.0%). The increase reflects continuing focus on improving capital returns by increasingly targeting higher added-value activities. On average, capital employed in 2013 was £304.2m (2012: £315.5m).

Achievements in 2013

The Group has continued to win business across all geographies. In both North America and Europe our ability to support automotive manufacturers as they move to newer technologies in pursuit of better fuel efficiency has provided Bodycote with market share growth. New outsourcing contracts and contributions from differentiated technologies such as S3P meant that the revenue declines stemming from the weak economic environment were mitigated and margins improved.

AGI continued to see the benefits of restructuring and market focus. The emphasis on improved efficiency has been a key factor in the achievement of margin enhancements in the face of declining revenues.

Organisation and people

At 31 December 2013, the number of full-time equivalent employees in AGI was 3,614 compared to 3,619 at the end of 2012 and 1,630 less than its peak in July 2008. AGI revenues of £357.8m compare to £363.3m in 2008 (at 2013 exchange rates), a decrease of 1.5%.

Looking ahead

The AGI businesses will continue to build on their success of enhancing their margins through capturing high value work. The focus on improving customer service helps drive this effort while the prioritisation of existing capacity in favour of higher value work and investing in selected technologies such as S3P, Corr-I-Dur® and low pressure carburising provides additional momentum. In addition the Group will continue with its strategy of adding to its existing footprint in emerging markets, with an emphasis on China and Mexico in the near term.

- Headline operating profit is reconciled to operating profit in note 2 to the financial statements. Bodycote plants do not exclusively supply services to customers of a given market sector (see note 2 to the financial statements).

AGI revenue by geography

£m

AGI revenue by market sector

£m